I hope this finds you well in the New Year. Below are my thoughts on the current market climate. Let me start by saying the economy looks strong, consumers continue to spend, inflation is slowly coming down, consumer confidence is trending up, unemployment remains low and many continue to travel and play catch up on… Read More

When Is The Next Stock Market Correction?

The stock market has been on a very strong run since the middle of 2016 with minimal volatility. As most long-term investors have experienced over the years, the market rarely keeps moving up for so long without some type of downward consolidation. I think this naturally begs the question – “when is the next stock… Read More

Ten Considerations If You Receive An Inheritance

At some point in your life you may receive an inheritance from a loved one or friend. There are a number of issues you should consider first before making any spending decisions: 1 – Don’t rush into any quick decisions You likely just lost someone close to you and, depending on the relationship, it could… Read More

Why Your Investments May Not Be Working For You

This article was written by a special guest author and colleague, Greg Geiger. Greg is a Principal of Financial Fiduciaries which is a fee-only investment advisory firm, registered with the National Association of Personal Financial Advisors (NAPFA), offering planning and investment services to individuals and institutions throughout Wisconsin. Our knowledgeable, experienced professionals serve as your advocate, helping… Read More

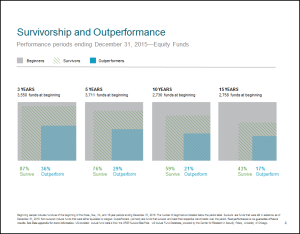

Survivorship Bias

Sports fans love to compare the sports heroes of their childhood era to current athletes and make a claim on who was the best ever. In many sports this claim on who was the best athlete of a particular time period can be subjective at best. However, baseball is one sport that allows for such… Read More

Emotional Bias in Investing

This article was written by a special guest author and colleague, Stephen Reh. Stephen Reh CFA, MBA, CFP® is the founder of Reh Weath Advisors LLC and https://investwithsteve.com/, a financial advisor in Southern California. Stephen is a member of the National Association of Personal Financial Advisors like David J. Fernandez, CFP® and specializes in financial planning and investment advice. Do you… Read More

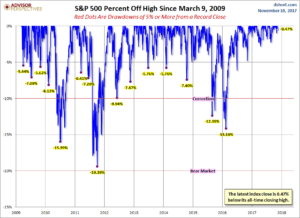

Two Key Benefits of Portfolio Diversification

Now that eight years have passed since the S&P 500 bottomed in March of 2009, I thought it would be a good time to revisit portfolio diversification. It’s easy to become complacent toward risk when the stock market keeps generally moving up from year to year. When times are good it is common that the… Read More

What’s The Best Way To Buy Gold?

As a continuation of the Fee-Only Financial Advisor blog sharing group, this month’s post comes to us from Joseph J. Alotta, a Financial Advisor in Oak Brook, Illinois. He shares his thoughts on how to purchase gold and silver coins for those investors preferring a small allocation of physical gold and silver. Admit it, you… Read More